Love or loathe it, insurance is a modern-day mainstay. With predictions suggesting that by 2030, a high percentage (some have suggested up to 90%) of all travelled miles will have been performed by autonomous electric vehicles, we take a quick look at what effect driverless cars will have on the automotive insurance industry as they become more prevalent on Australian roads.

To get an idea of where the Australian automotive industry might be headed, let’s take a look at Tesla.

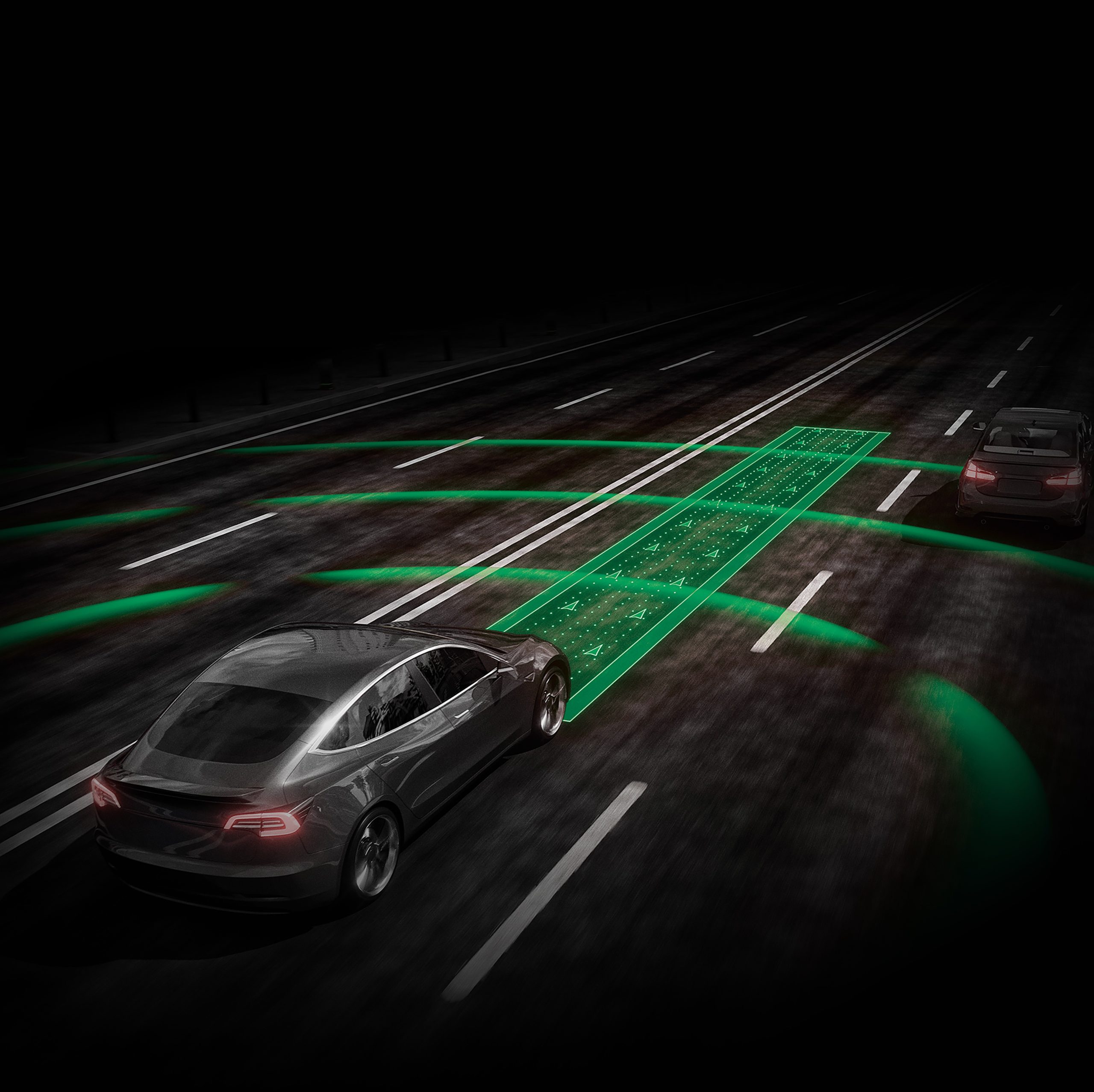

Currently at the forefront of national debate around insurance premiums in the US, the company believes that premiums should be adjusted to account for the fact that driverless cars are safer.

In fact, there is evidence to support Tesla’s stance. The National Highway Traffic Administration found that accident rates for the company’s driverless cars have plummeted 40% since proprietary technology was installed in 2015.

If statistics prove that self-driving cars can reduce the number of collisions, most people could be forgiven for assuming this should also mean a reduction in insurance premiums.

Assumptions like these are in line with industry observers who believe that the insurance industry will be hit hard by autonomous cars. According to a report by the global accounting firm KPMG, autonomous vehicles could shrink the auto-insurance sector by a significant percentage over the next 25 years.

WHO’S AT FAULT?

While opinions vary, experts do agree that ‘Level 4’ or ‘Level 5’ self-driving cars, which refers to vehicles that can perform without human interaction whatsoever, remove all blame from the individual and put it on the manufacturer. In this way, emphasis is placed on how a computer was programmed and how the vehicle was instructed to operate to determine the cause, and blame, for an accident.

A precedent has already been set for automakers to take full responsibility. Google and Ford recently announced plans to roll out a range of driverless cars that have been designed with the steering wheel and pedals removed.

Volvo went further in 2015 by going on record to say it will accept full liability in the event its self-driving car gets into an accident.

WHERE TO FROM HERE?

While speculation abounds, no-one can say for sure what effect autonomous vehicles will have on the insurance industry in Australia.

Perhaps it might take on a no-fault form, in which neither party is at fault, and each car owner’s insurance covers their own vehicle, thereby becoming like a utility bill with the fee based on usage. Of course, that is just a guess.

Whichever model rises to the surface in the coming months and years, one thing we can be certain of is that insurers will have to react sooner rather than later in order to meet consumer needs in this changing space.